News

The Benefits of Custom Home Construction: Why Personalization Matters

Congratulations on building your new home! Now that you have your dream home, it's essential to take proper care of it to ensure it stays in top shape for years to come. Regular home maintenance not only helps preserve the aesthetics but also prevents costly repairs down the line. In this blog post, we'll provide you with five examples of essential home maintenance tasks to help you keep your new home in pristine condition.

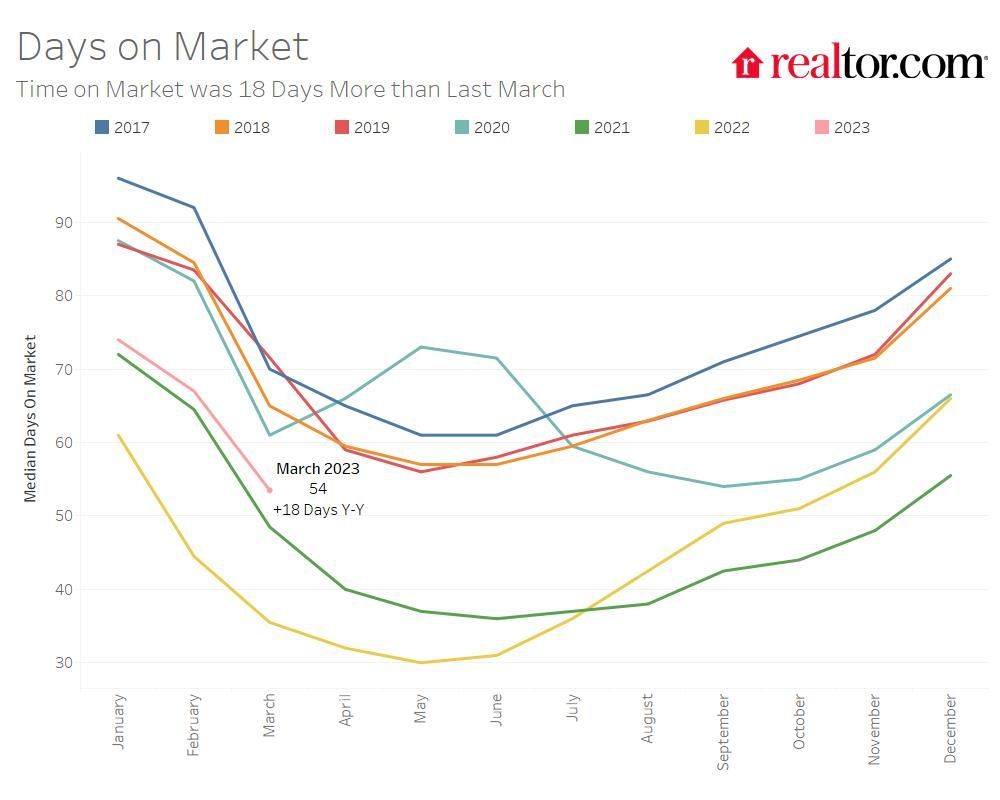

Spring is typically a busy time for the real estate market, and 2023 is no exception. However, there are some key trends that are shaping the market and making it an interesting time for buyers and sellers alike. Here are three key points to keep in mind about the spring real estate market.

2022 Home for the Holidays Promotion

3 Reasons to Build a Home This Fall

Fall is here, with leaves starting to turn, cool winds blowing, and that home decorating itch that comes for many homeowners during the changing of the seasons. With endless styling options to use in your home, we’ve compiled a list of six fall home decor trends that interior designers are using in 2022.

Achieving Your Homeownership Goals Using Your Tax Refund

Where are Mortgage Rates Headed Next?

Helpful Terms for Homebuyers